The Zombie Unicorn Was Never the Point

AI-native services are wiping out a generation of SaaS unicorns, and most people are reading it as the death of software. It is not. It is the death of one shape of software, the generic VC-scale kind, and the winners are the operators who can now build a small, profitable, un-funded product in a niche they actually understand.

AI-native services are wiping out a generation of SaaS unicorns, and most people are reading it as the death of software. It is not. It is the death of one shape of software, the generic VC-scale kind, and the winners are the operators who can now build a small, profitable, un-funded product in a niche they actually understand.

Opening scene

I build AI-native companies for a living, so when people send me the latest fallen-unicorn list with a worried note, they expect me to flinch. I don't. I have spent the last few years watching the cost of building a working product fall through the floor, and I keep landing on the same thought. The thing dying in those headlines is not software. It is a specific business that used to need a lot of money to exist. Stack Overflow makes the point better than any chart. The forum is effectively dead, question volume back to where it was in 2009, yet the company survives by licensing its archive to the AI that killed it. So here is the question I want to sit with. What exactly are we mourning?

The barbell

I think of it as the barbell. On one end you have hyperscale AI-native players absorbing generic, horizontal functionality. On the other end you have tiny, owned, profitable software built by someone who lives inside a specific industry. Both ends are healthy. The middle is where the bodies are. That middle is the VC-scale generic SaaS unicorn, the one that charged per seat, raised every eighteen months, and sold undifferentiated workflow to everyone. The barbell has two outcomes for any product you build. Either you are heavy enough to be infrastructure, or you are sharp enough to be irreplaceable in one niche. If you are neither, you are standing in the part of the bar that snapped.

The uncomfortable version

Here is the part I have to say to myself first. Cheap building does not mean everyone wins. I was trained, like every founder, to chase the billion-dollar number, and that ambition is now the trap, not the goal. The cleanest death in this whole story proves it. Chegg built its own AI tool on OpenAI's API, which made it indistinguishable from OpenAI, so customers had no reason to pay. If I build on top of the labs without bringing my own judgment, I am Chegg. The valuation never protected anyone. It just hid the absence of a moat for a few more quarters.

The reframe

So the shift is simple. The unicorn was never a measure of value. It was a measure of how expensive building used to be. You needed venture money to hire the engineers, so you needed a venture-scale outcome to justify it, so you optimized for a mark instead of a margin. Building got cheap. The whole chain dissolves. A profitable micro-SaaS you own outright is not the consolation prize for failing to raise. In an AI-native market, it is the better outcome, and it always was.

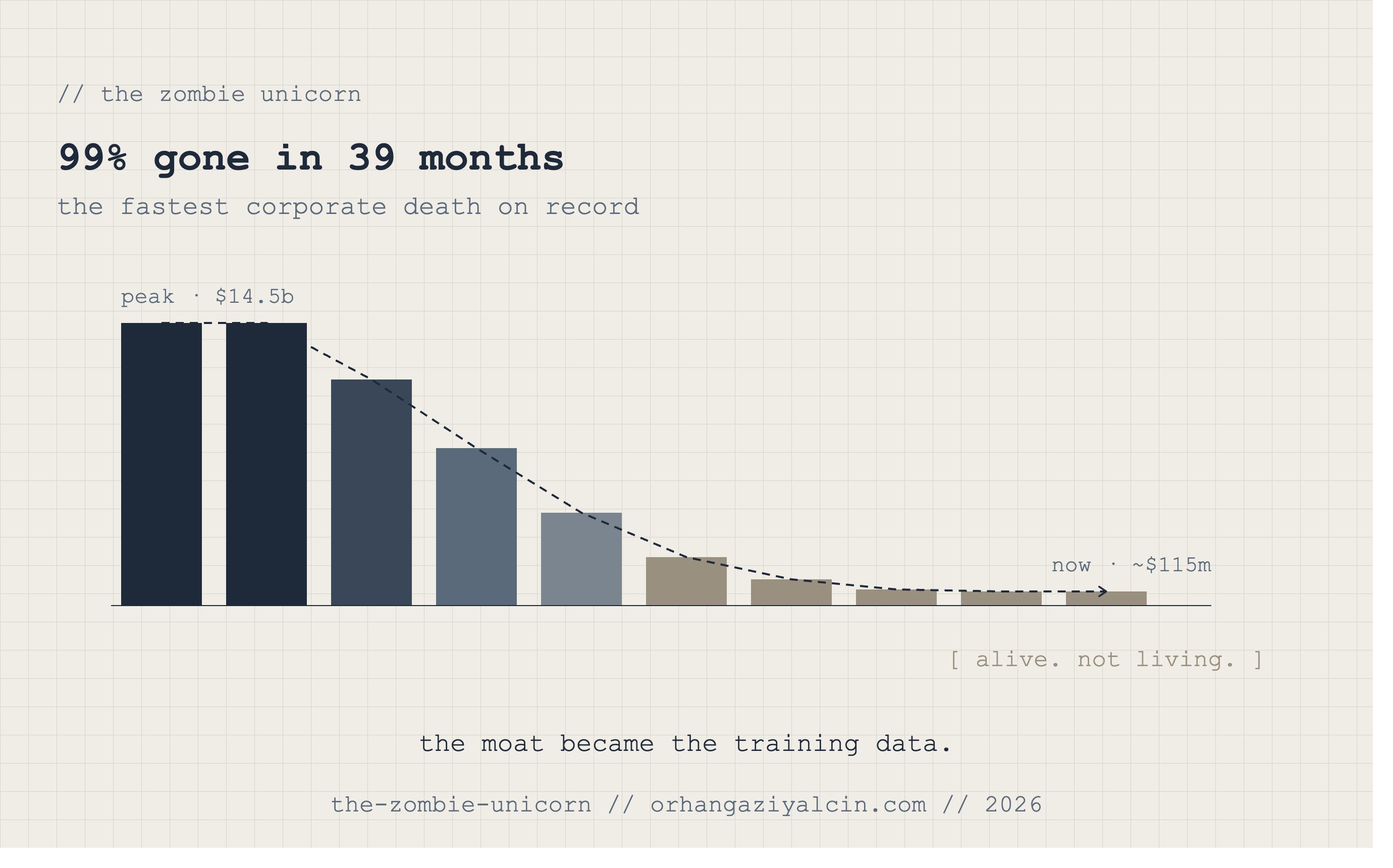

Go looking

Go looking and the pattern is everywhere. Chegg spent a decade paying contractors to build 79 million homework answers and charged students twenty dollars a month for access. That moat compounded value in the old world and inverted the moment intelligence got free, taking 99 percent of the company's value with it. Stack Overflow's question volume has fallen more than 75 percent from its peak, and the only asset left with value is the archive it now sells to LLM providers. Jasper is the nuance. It is not dead, it just re-rated, an AI company priced as a unicorn and then quietly squeezed by cheaper AI from labs like DeepSeek. Then there is the broad cohort. More than 220 companies have dropped below the billion-dollar mark, 75 of them SaaS, the largest single category, and the 2021 vintage is worth roughly 68 percent less on average. Calendly sits among the prominent names. The mechanism underneath all of it shows up in one question investors now ask every legacy software pitch. Why can't OpenAI, Anthropic, or Google just do this. For the generic middle, the honest answer is that they can. The old safety net is gone too. The two-million-dollars-per-engineer acquisition floor that used to guarantee a soft landing collapsed once small teams started shipping with AI tooling. One caveat, so I stay honest. Those lists are padded with direct-to-consumer brands like Glossier and The Farmer's Dog that died of interest rates, not AI. Separate the product deaths from the stale valuations or the argument goes soft.

The table

| The VC-Scale Unicorn (commoditizing) | The Owned Micro-SaaS (compounding) |

|---|---|

| Seat-based pricing | The outcome you actually deliver |

| Raw intelligence rented from a lab | Domain judgment that compounds |

| Built by a funded engineering org | Built by one operator who lived the problem |

| Weaker as the models improve | Stronger as the models improve |

| Owned by investors, chasing a mark | Owned by you, chasing a margin |

| Horizontal and generic | Narrow and specific |

Read top to bottom, the left column is everything AI now commoditizes, and the right column is everything it cannot touch.

Why it passes

This is why the micro-SaaS passes the test the unicorn fails. When raw intelligence becomes a commodity you rent by the token, the only durable moat is the judgment around it. Reading what a customer actually needs from incomplete signals. Knowing which problem in your industry is worth solving and which is noise. Connecting the output to the messy, non-automated reality on the other side. That judgment compounds with experience and cannot be rented from a lab. So the better the models get, the more valuable your product becomes, because the model does more of the cheap work and your judgment does more of the expensive work. The unicorn fails the same test for the opposite reason. Its moat was the intelligence itself, and that is precisely what got commoditized.

Three reader questions

- Does your product get stronger or weaker as the models improve? If a smarter model makes you more valuable, you are building a durable asset. If it makes you redundant, you are building a zombie.

- Are you building the generic middle, or a niche you have actually lived? The middle is where every undifferentiated tool is going to die. Specific, hard-won domain knowledge is the part no lab can copy.

- Do you really need the venture money, or did building just used to be expensive? Be honest about whether you are chasing a valuation out of habit, when ownership and profit are now within reach without it.

Closing kicker

The zombie unicorns are not the death of software. They are a permission slip. Build something small, build it on judgment the models cannot rent, and own the whole thing.